consolidation may become unavoidable despite strong overallperformance. In the foreword to its March 2026 Financial Stability Report, Eyob Tekalign, Governor of the National Bank of Ethiopia (NBE), underscores that the sector is currently operating from a position of strength — but warns that its structure is increasingly difficult to sustain.

The Paradox of Strength

The Paradox of Strength

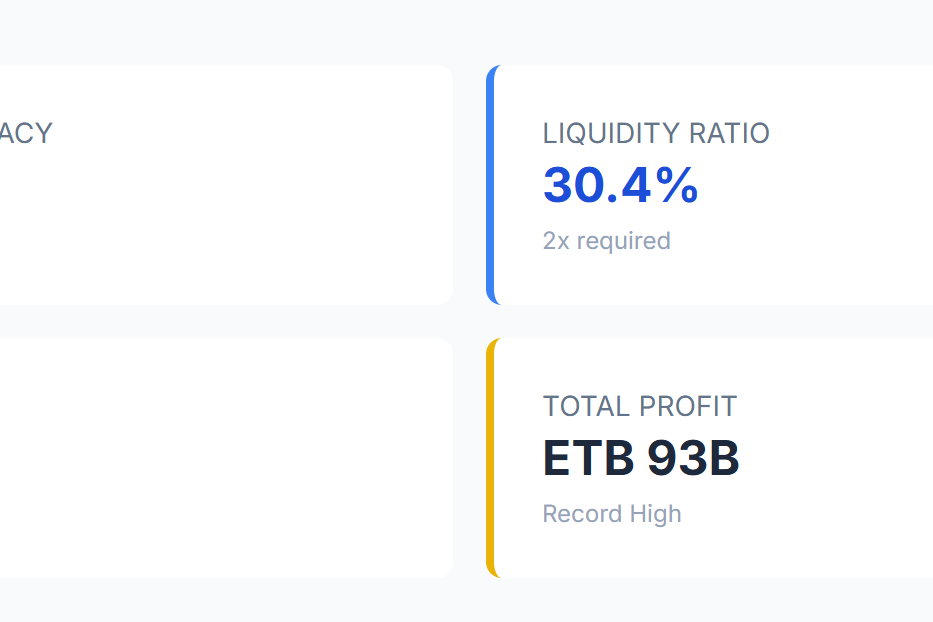

The report is explicit: Ethiopia does not have a weak banking sector. It is described as “stable, resilient, and low risk.” However, this stability masks a profound structural imbalance. While system-level capacity is robust, the distribution of that capacity is increasingly skewed.

“Increasing market concentration and widening performance gaps across institutions are becoming evident — highlighting the continued need for efficiency enhancements, innovation, and in some cases, consolidation,” the Governor wrote.

Survival Pressure: The “Fittest” Mandate

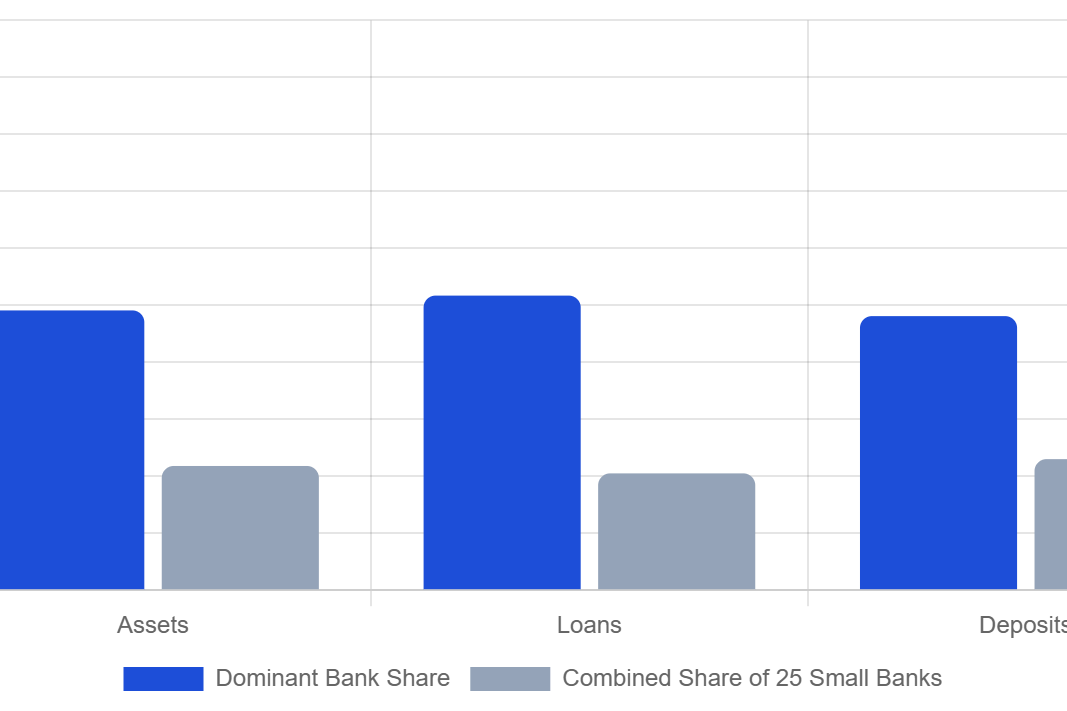

Perhaps the most significant signal from the NBE is not about stability, but about survival. The report notes that “only the fittest institutions will survive” — policy signalling language that indicates the 25 smaller banks, which together hold only approximately 21.8 percent of system assets, are facing an existential efficiency gap.

The warning is directed at institutions that, despite remaining technically solvent, lack the scale, technology, and operational efficiency to compete in a liberalising market.

Drivers of Consolidation

Drivers of Consolidation

Three structural forces are driving the consolidation pressure:

Market Dominance — the single systemically important bank is growing its footprint faster than the rest of the market combined, pulling capital, deposits, and talent toward the top of the sector.

Fragmentation — 25 banks competing for less than a quarter of the market is economically inefficient, limiting their ability to invest in technology, expand branch networks, or absorb shocks.

Legal Readiness — new banking laws now explicitly include mergers and acquisitions as part of the formal crisis management framework, creating a regulatory pathway for restructuring that did not previously exist.

The Road to Restructuring

While the language stops short of mandating mergers, it marks the clearest indication yet that parts of Ethiopia’s fragmented banking landscape may need to restructure. The message is reinforced by ongoing regulatory reforms, positioning consolidation as a policy-supported pathway rather than a forced intervention.

The fate of most small banks is not failure due to instability, but forced restructuring due to inefficiency and scale disadvantage — a distinction the NBE appears to be making deliberately.

The National Bank’s report signals that while Ethiopia’s banking sector is strong, its structure is unsustainable. With one bank controlling half the market and 25 others sharing less than a quarter, consolidation is no longer optional — it is inevitable.