The global aviation industry recorded its sharpest traffic shock since the post-pandemic recovery began after war-driven disruptions in the Middle East triggered a collapse in regional air travel and pushed worldwide passenger demand into negative territory.

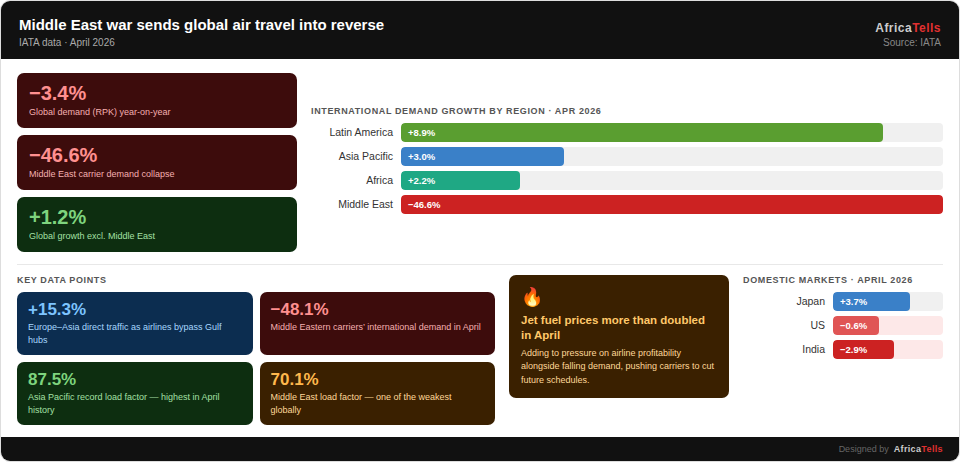

According to new data released by the International Air Transport Association (IATA), global passenger demand measured in revenue passenger kilometers (RPK) fell 3.4% year-on-year in April 2026. The decline was overwhelmingly driven by the Middle East, where carriers saw demand plunge by 46.6% amid the ongoing Iran war and regional instability.

Excluding the Middle East, global passenger demand would have grown by 1.2%, highlighting how concentrated the shock has become.

“The 46.6% fall in demand for carriers in the Middle East due to war in the region was so acute that it dragged overall demand down 3.4%,” said Willie Walsh, IATA’s Director General.

War Reshapes Global Air Corridors

The aviation downturn reflects more than falling passenger confidence. The conflict has disrupted long established transit routes linking Europe, Asia, and Africa through Gulf aviation hubs, forcing airlines to reroute aircraft, shorten schedules, and absorb sharply higher fuel costs.

Middle Eastern airlines reported a 48.1% collapse in international demand in April, while capacity fell 38.4%. Passenger load factors dropped to 70.1%, one of the weakest performances globally.

The disruption is already reshaping international traffic flows. IATA noted that direct Europe-Asia traffic increased by 15.3% as airlines and passengers avoided Middle Eastern transit corridors.

That shift suggests a structural rerouting of global aviation networks, particularly for long-haul intercontinental traffic that previously relied heavily on Gulf mega hubs.

At the same time, political tensions in East Asia are beginning to influence regional mobility patterns. IATA reported a “notable slowdown” in traffic on the Japan-China corridor amid ongoing geopolitical strains.

Fuel Shock Adds New Pressure

The aviation slowdown is also colliding with a sharp increase in operating costs.

Jet fuel prices more than doubled in April, according to IATA, increasing pressure on airline profitability and pushing carriers to reduce future schedules.

“The situation for air transport remains highly volatile,” Walsh said. “Forward schedule data is showing a reduced offering in the coming months, indicating that airlines are balancing high fuel costs and weaker demand.”

The dual shock of falling demand and rising fuel costs creates a particularly difficult environment for airlines already operating on thin margins. Analysts warn that carriers may increasingly cut frequencies, retire less profitable routes, and raise fares to preserve cash flow.

Africa Holds Positive Momentum

Despite global turbulence, African airlines remained in positive territory.

African carriers recorded a 2.2% increase in international passenger demand in April, while capacity rose 1.2%. Passenger load factors improved to 77.9%.

Although Africa represents only 2.2% of global air traffic, the region’s continued growth suggests that intra-African mobility and recovering tourism demand are partially insulating the continent from broader global aviation volatility.

Latin America also posted strong gains, with demand rising 8.9%, making it the fastest growing international market during the month.

Asia Pacific carriers reported 3% growth and achieved a record April load factor of 87.5%, indicating that underlying travel demand across much of Asia remains resilient despite geopolitical uncertainty.

Domestic Markets Lose Momentum

Domestic passenger markets showed signs of stagnation.

Global domestic demand was flat year-on-year, with weakness in major aviation markets including the United States, India, and Australia offsetting growth in China, Brazil, and Japan.

The US domestic market, which accounts for 13.6% of global RPKs, recorded a 0.6% decline in demand. India also posted a 2.9% contraction despite continued aviation expansion efforts.

Japan stood out as an exception. Domestic demand rose 3.7% even as airlines reduced capacity for an eighth consecutive month, helping improve load factors significantly.

The April figures underline how quickly geopolitical conflict can ripple through global aviation markets, affecting not only regional carriers but international pricing, route structures, fuel economics, and passenger behavior worldwide.